Betterment vs. Wealthfront vs. Schwab: Robo-Advisor Review

Introduction: The Maturation of the Algorithmic Advisory Sector

By the first quarter of 2026, the digital wealth management industry—colloquially recognized as the robo-advisor sector—has completely transitioned from a disruptive financial technology novelty into a foundational, commoditized pillar of modern retail investing. Pioneered in the late 2000s during the fallout of the global financial crisis by independent financial technology firms like Betterment and Wealthfront, the model of algorithmically driven, low-cost portfolio management has since been universally adopted and scaled by legacy institutions. The Charles Schwab Corporation represents the most formidable incumbent in this space, leveraging its massive existing brokerage infrastructure to capture substantial market share through its Schwab Intelligent Portfolios product. This report provides an exhaustive, highly nuanced comparative analysis of the three dominant platforms in the 2026 landscape: Betterment, Wealthfront, and Schwab Intelligent Portfolios.

The core value proposition of these platforms remains consistent across the industry: the democratization of Modern Portfolio Theory (MPT), automated portfolio rebalancing, and algorithmic tax optimization, all delivered at a fraction of the cost associated with traditional human financial advisors. For decades, access to sophisticated tax-loss harvesting and custom index construction was gated behind high net-worth minimums and exorbitant advisory fees frequently exceeding 1.00% of Assets Under Management (AUM). The algorithmic revolution engineered by Betterment and Wealthfront, both founded in 2008, compressed these fees to a baseline of roughly 0.25%, forcing legacy institutions to respond. As of the mid-2020s, Betterment manages over $56 billion in assets across more than 900,000 customer accounts, while Wealthfront manages over $37.4 billion across more than 500,000 clients, with Schwab managing vast sums within its proprietary automated ecosystem.

However, as the market has matured into 2026, the architectural philosophies of these three platforms have diverged significantly. Investors are no longer merely choosing between largely identical mean-variance optimization algorithms; rather, they are selecting between fundamentally different economic revenue models, varying degrees of tax-optimization sophistication, and highly distinct structural service offerings. The decision matrix now encompasses variables such as explicit advisory fees versus implicit cash drag, daily tax-loss harvesting versus periodic secondary ETF rotation, the proliferation of direct indexing capabilities, and the integration of alternative asset classes such as spot cryptocurrency Exchange-Traded Funds (ETFs) and Environmental, Social, and Governance (ESG) mandates.

Furthermore, the global nature of modern capital flows necessitates an examination of these platforms through an international lens. This analysis specifically addresses the critical global jurisdictional constraints facing expatriates and international investors—specifically in regions such as Nepal—who seek access to U.S.-domiciled automated portfolios in 2026. The global financial regulatory landscape, heavily influenced by frameworks such as the Foreign Account Tax Compliance Act (FATCA), has severely restricted cross-border wealth management, creating distinct accessibility firewalls among these providers.

Through a rigorous examination of the underlying 2026 data, this report isolates the comparative advantages, structural limitations, and subtle opportunity costs inherent in Betterment, Wealthfront, and Schwab Intelligent Portfolios. By synthesizing fee architectures, fixed-income innovations amidst fluctuating interest rate environments, and direct indexing methodologies, this analysis provides a definitive, expert-level roadmap for optimal capital allocation within the contemporary automated advisory ecosystem.

Macro-Structural Shifts: The 2026 Discontinuation of Schwab Intelligent Portfolios Premium

A defining macroeconomic and structural event in the 2026 digital wealth management landscape was Charles Schwab’s decision to formally discontinue its hybrid advisory tier, Schwab Intelligent Portfolios Premium. Understanding this strategic retreat is essential for contextualizing the current competitive dynamics between the three major providers, as it signals a broader industry realization regarding the unit economics of human-augmented digital advice.

Previously, Schwab operated a bifurcated automated advisory model. The foundational tier, Schwab Intelligent Portfolios, offered fully automated ETF management with no explicit advisory fee. For clients seeking human intervention, Schwab offered the Premium tier, which required a $25,000 minimum balance and charged an initial $300 financial planning setup fee followed by a $30 monthly subscription. This Premium tier was highly notable for providing clients with unlimited access to Certified Financial Planners (CFPs), representing a robust hybrid robo-advisory approach designed to compete directly with Vanguard Personal Advisor Services and Betterment’s own Premium offering.

The retirement of this hybrid tier in the first quarter of 2026 underscores the escalating labor and compliance costs associated with maintaining a vast network of human fiduciaries to service mass-affluent accounts. Schwab transitioned existing Premium accounts down to the standard Schwab Intelligent Portfolios tier, thereby eliminating the $30 quarterly/monthly subscription fee while simultaneously revoking access to the unlimited CFP consultation sessions. Industry analysts have interpreted this move as a capitulation to the margin pressures inherent in the hybrid model, leading to broad declarations from financial commentators that the traditional “robo-advice era”—specifically the era in which digital platforms attempted to replicate full-suite, bespoke human financial planning at severe discount prices—is undergoing a fundamental realignment.

This strategic pivot by a legacy behemoth heavily alters the comparative dynamics and value propositions among the three evaluated providers. Schwab Intelligent Portfolios is now strictly a fully automated, human-less digital offering. Wealthfront, maintaining its historical reliance on pure software-driven financial engineering, continues to eschew human advisors entirely in favor of advanced digital pathing, algorithms, and deep automation. Consequently, Betterment remains the sole provider among these three specific platforms to actively support a hybrid human-digital model in 2026. Betterment’s Premium plan charges an explicit 0.65% annual advisory fee for unlimited CFP access, provided the client meets a stringent $100,000 minimum account balance.

The dissolution of Schwab’s Premium tier proves that offering unlimited human advice at scale via a low-cost subscription model is economically fragile. Investors in 2026 who possess high portfolio balances and demand human fiduciary intervention are now structurally funneled toward Betterment Premium. Conversely, investors who are comfortable with purely algorithmic management must evaluate the explicit, software-focused fee model of Wealthfront against the implicit, cash-heavy monetization model of the standard Schwab tier.

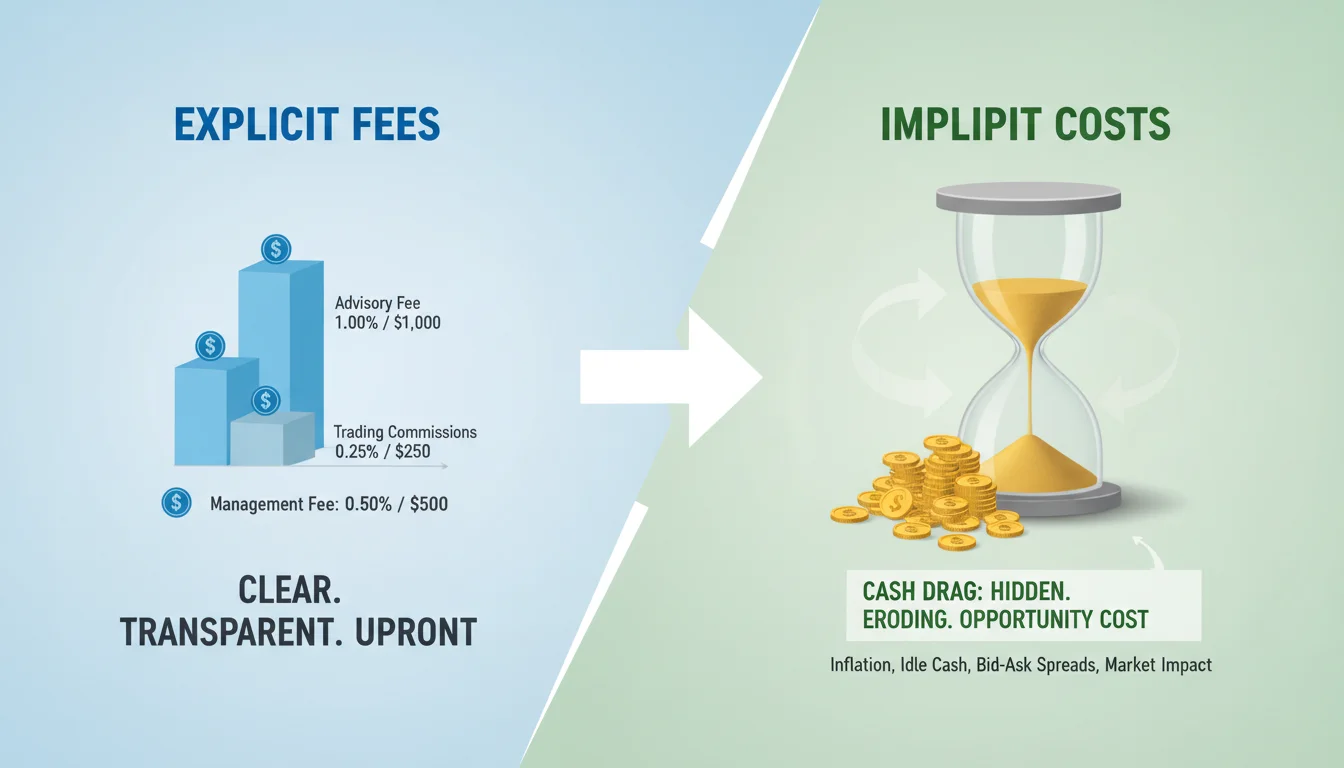

Fee Architectures and Economic Models: Explicit Costs vs. Implicit Cash Drag

The most profound, yet frequently misunderstood, divergence among Betterment, Wealthfront, and Schwab Intelligent Portfolios lies in how these corporate entities generate revenue. While the industry standard baseline automated advisory fee has largely consolidated around 0.25% of Assets Under Management (AUM), the actual mechanisms of fee assessment vary radically, particularly when contrasting the models of independent financial technology firms against those of legacy retail brokerages.

Betterment: Tiered Explicit Pricing and Micro-Account Friction

Betterment utilizes an explicit fee structure, but one characterized by tiered complexities based on account size, household aggregation, and deposit velocity. The platform’s standard digital offering carries a baseline advisory fee of 0.25% annually.

However, Betterment implements a pricing mechanism that effectively penalizes low-balance, inactive accounts. For retail investors with an aggregate household balance under $20,000 (or $24,000 depending on the specific promotional tiering in effect), Betterment charges a flat $4 to $5 monthly maintenance fee.

To avoid this flat fee and revert to the standard 0.25% AUM pricing, the investor must initiate recurring monthly deposits or transfers totaling at least $250 across their Betterment accounts. While seemingly nominal, a $5 monthly fee on a $1,000 account translates to a 6.00% annual fee drag, representing a massive frictional cost that destroys long-term compounding. This structure explicitly forces micro-account holders and novice investors to either automate their savings behavior or face punitive percentage fees.

For high-net-worth investors, Betterment offers fee compression.

If an eligible household investing balance exceeds $1 million, the marginal fee drops to 0.15% on the portion of assets between $1 million and $2 million, and further compresses to 0.10% on the portion of assets exceeding $2 million. The Premium tier, requiring a $100,000 minimum, charges a flat 0.65% annually to cover the automated management alongside unlimited CFP access. Furthermore, transferring assets away from Betterment incurs a flat $75 outbound transfer fee per investing account.

3.2 Wealthfront: The Pure Flat-Fee Software Model

In stark contrast to Betterment’s tiered complexity, Wealthfront’s pricing architecture is defined by rigid, transparent simplicity. Since its founding, the firm has maintained a flat 0.25% annual advisory fee across all of its automated investing portfolios, automated bond portfolios, and automated bond ladders. Wealthfront requires a higher baseline minimum account balance of $500 for its automated investment accounts, but it does not employ punitive monthly subscription fees for low balances, nor does it offer high-balance fee compression discounts for multi-million dollar accounts.

The 0.25% fee is deducted monthly and comprehensively covers all algorithm trading, systematic rebalancing, and standard tax-loss harvesting execution. Wealthfront generates additional ancillary revenue through its advanced Direct Indexing portfolios, which charge highly competitive advisory fees for index reconstruction: 0.09% for the S&P 500 Direct portfolio and 0.12% for the Nasdaq-100 Direct portfolio. Demonstrating a commitment to loss-leader client acquisition, Wealthfront also operates a purely self-directed Stock Investing Account with absolutely zero advisory fees, zero account fees, and zero commissions, while explicitly refusing to accept Payment for Order Flow (PFOF).

3.3 Schwab Intelligent Portfolios: The Implicit Cash Allocation Model

Schwab Intelligent Portfolios is aggressively and prominently marketed as a “zero advisory fee” platform. The service charges no explicit management fees and levies no trading commissions, creating a highly compelling optical advantage over its fintech rivals. The minimum entry requirement is a relatively steep $5,000.

However, the economic reality of the Schwab model relies heavily on implicit costs—specifically, a mandatory, non-negotiable cash allocation. Schwab’s portfolio optimization algorithms require a significant portion of every client portfolio to be held in uninvested cash. Depending on the client’s stated risk tolerance, this cash allocation typically ranges from a minimum of 6% for aggressive investors to upwards of 30% for conservative portfolios. These cash reserves are automatically swept into FDIC-insured Deposit Accounts at Charles Schwab Bank, SSB.

This cash drag acts as Schwab’s primary monetization engine for the Intelligent Portfolios product. Schwab Bank earns net interest margin by lending out or investing these aggregated deposit balances at higher institutional rates, while paying the retail investor a lower internal yield. The platform’s own disclosures explicitly state that Schwab does not charge an advisory fee in part because of the revenue Schwab Bank generates from this cash allocation, acknowledging it as an “indirect cost of the Program”. Furthermore, the disclosures note that the interest rate paid to clients on this cash might be significantly lower than yields available in money market funds or high-yield alternatives outside the program.

The mathematical consequence of this structure is profound. In sustained equity bull markets or high-inflation environments, the mandatory cash allocation severely dilutes the overall equity risk premium of the portfolio. The opportunity cost of missing out on equity returns (or higher-yielding fixed-income returns) on 6% to 30% of the total portfolio value can frequently exceed the explicit 0.25% fee charged by Betterment or Wealthfront. While the zero-fee optical illusion is appealing, sophisticated investors must calculate the performance drag of idle capital when evaluating Schwab’s true cost of ownership.

3.4 ETF Operating Expense Ratios

Beyond the platform-level advisory fees, investors on all three platforms must bear the internal operating costs of the underlying Exchange-Traded Funds utilized to construct the portfolios. These fees, known as Expense Ratios (ER), are deducted directly from the fund’s Net Asset Value (NAV) by the ETF issuer (e.g., Vanguard, iShares, State Street) and are not paid to the robo-advisor, with the notable exception of Schwab.

The platforms rigorously screen for low-cost funds to minimize this internal drag. Betterment’s Core automated portfolios average an ETF expense ratio ranging from 0.04% to 0.11%. Wealthfront’s automated portfolios report slightly broader average ETF expense ratios, typically varying between 0.06% and 0.15% depending on the specific asset class exposure.

Schwab Intelligent Portfolios boasts the lowest underlying fund costs, utilizing portfolios with expense ratios generally landing between 0.03% and 0.05%. However, it is critical to note that Schwab’s algorithm heavily prioritizes its own proprietary Schwab ETFs alongside third-party funds. When a client’s portfolio utilizes a Schwab ETF, a Schwab affiliate (Charles Schwab Investment Management, Inc.) receives the internal management fees on those ETFs, creating a secondary, internalized revenue stream for the broader corporation. Schwab also receives compensation from third-party ETF providers for shareholder services and order flow routing, highlighting the multi-faceted monetization strategy underpinning the “free” service.

Table 1: Comparative Fee and Minimum Architecture

| Feature / Metric | Betterment | Wealthfront | Schwab Intelligent Portfolios |

|---|---|---|---|

| Minimum Investment | $0 (Digital), $100k (Premium) | $500 (Automated), $1 (Cash/Stock) | $5,000 |

| Standard Advisory Fee | 0.25% (or $4-$5/mo if <$20k) | 0.25% flat | 0.00% (No explicit fee) |

| Premium / Hybrid Tier | 0.65% (Unlimited CFP access) | N/A (Digital software only) | Discontinued in 2026 |

| Average ETF Expense Ratio | ~0.04% – 0.11% | ~0.06% – 0.15% | ~0.03% – 0.05% |

| Monetization Mechanism | Explicit AUM fees, Subscription fees | Explicit AUM fees, Direct Index fees | Net Interest Margin on Cash, Internal ETF ERs |

4. Portfolio Construction, Customization, and Fractional Efficiencies

While all three robo-advisors utilize the foundational principles of Modern Portfolio Theory—attempting to optimize for the highest expected return at a given level of risk via the Efficient Frontier—their practical execution of asset allocation, index selection, and trade mechanics differ substantially. These differences dictate how tightly tracking error is managed and how efficiently capital is deployed.

4.1 Betterment: Goal-Based Optimization and Fractional Trading

Betterment’s portfolio architecture is intrinsically tied to a philosophy of “Goal-Based Investing.” Rather than maintaining a single monolithic investment account, users are encouraged to create separate, compartmentalized sub-portfolios for distinct financial objectives (e.g., “Retirement,” “House Down Payment,” “Safety Net,” “Child’s Education”). The algorithm automatically designs a specific risk profile and “glide path” for each goal. As the target date for a specific goal approaches, the software systematically de-risks the sub-portfolio, automatically shifting capital allocations away from volatile equities and into stable fixed-income assets to preserve capital.

Betterment constructs its Core portfolio utilizing up to 12 distinct asset classes, providing broad global diversification. A major structural advantage of Betterment’s execution engine is its universal implementation of fractional share investing across all portfolios. This mechanical feature ensures absolute zero cash drag; every single cent deposited by the client is immediately and mathematically allocated to the target asset weights down to the micro-decimal, maximizing time-in-market.

However, Betterment is highly restrictive regarding user-level customization. To maintain strict adherence to its strategic asset allocation models and risk parameters, Betterment prevents clients from picking individual ETFs or customizing the underlying funds within the automated portfolios. Clients can adjust top-level macro allocations (e.g., shifting the ratio of stocks to bonds), but the underlying constituent ETFs are locked by Betterment’s investment committee.

4.2 Wealthfront: Deep Customization and Risk Parity

Wealthfront offers a more expansive array of asset classes, utilizing up to 17 global asset classes in its automated accounts to achieve deep diversification. While Wealthfront also embraces MPT, it leans heavily into advanced, institutional-grade strategies. Most notably, for accounts exceeding $500,000, Wealthfront offers Risk Parity, marketed as Smart Beta. Risk Parity strategies attempt to equalize the risk contribution of different asset classes within the portfolio, rather than strictly weighting them by capital allocation. This often involves leveraging lower-volatility assets (like bonds) to balance the volatility profile of equities, creating a theoretically smoother return trajectory during turbulent market conditions.

Unlike Betterment’s rigid walled garden, Wealthfront allows extensive ETF-level customization. Clients are empowered to build portfolios entirely from scratch or intricately modify the firm’s curated portfolios by adding, removing, or adjusting the percentage weights of hundreds of supported ETFs and specific asset classes. This allows experienced investors to tilt their portfolios toward specific sectors, such as clean energy or emerging markets, while still benefiting from automated rebalancing.

Furthermore, Wealthfront achieved mechanical parity with Betterment by successfully rolling out fractional shares across its Automated Investing Accounts, IRAs, and Automated Bond Portfolios in late 2025 and early 2026, effectively eliminating uninvested cash drag outside of its separate checking features.

Schwab: Fundamental Weighting and Maximum Breadth

Schwab Intelligent Portfolios takes the most diverse approach to raw asset class inclusion, offering over 80 portfolio variations that span up to 20 distinct asset classes. Schwab differentiates its construction methodology by utilizing a blend of traditional market-capitalization-weighted ETFs and fundamentally weighted ETFs. Fundamental weighting constructs indices based on underlying corporate economic metrics—such as total sales, cash flow, and dividends—rather than simply stock price. Schwab’s investment committee argues this methodology provides a structural hedge against market bubbles and overvalued mega-cap tech stocks that dominate cap-weighted indices.

However, Schwab suffers from mechanical friction because it does not offer fractional share trading within its Intelligent Portfolios. Consequently, whenever dividends are paid or deposits are made, small residual cash balances that are insufficient to purchase whole shares remain uninvested. This friction compounds alongside the previously discussed mandatory strategic cash sweep allocation. Furthermore, user customization is highly restricted compared to Wealthfront; clients cannot hand-pick underlying ETFs or dictate percentage allocations, though they are permitted to manually exclude up to three specific ETFs from their portfolio to avoid unwanted exposures.

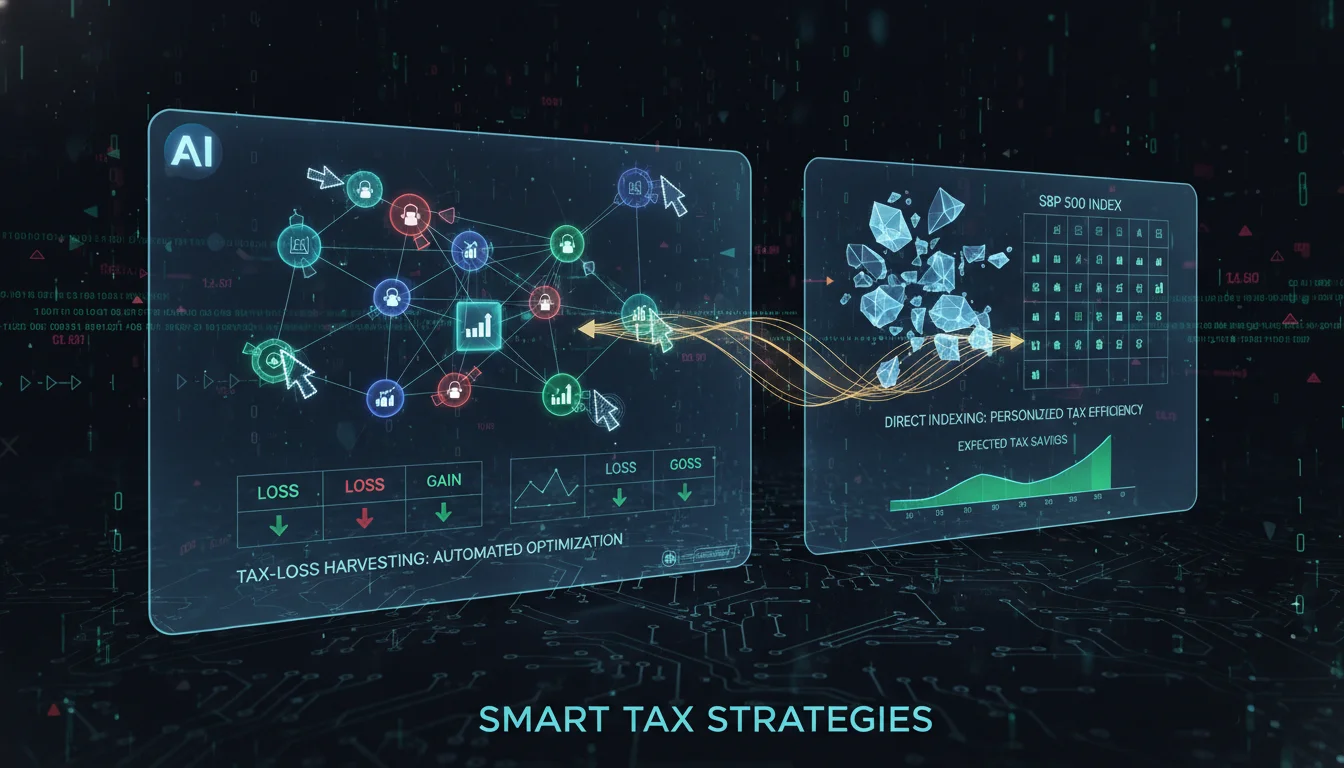

Tax Optimization: The Vanguard of Tax-Loss Harvesting and Direct Indexing

The ability to mathematically generate “tax alpha”—excess returns derived purely from tax efficiency rather than asset outperformance—is the single most compelling justification for paying a robo-advisor’s explicit advisory fee. Tax-Loss Harvesting (TLH) is an automated strategy that involves intentionally selling assets that have declined below their original cost basis. This action realizes a capital loss, which can then be used to offset realized capital gains elsewhere in the portfolio, or offset up to $3,000 of ordinary income annually under U.S. tax code. The algorithm immediately reinvests the proceeds from the sale into a highly correlated, but not “substantially identical,” alternative asset. This maintains the portfolio’s target risk profile and market exposure while successfully navigating IRS wash-sale violations.

Wealthfront: The Zenith of Automated Tax Alpha

Wealthfront’s proprietary tax-optimization software is widely considered the gold standard and benchmark of the industry. Wealthfront executes TLH daily across all taxable accounts at no additional cost, with no minimum balance required to unlock the feature. According to the firm’s exhaustive 2026 research whitepapers, their automated TLH strategy pays for the 0.25% advisory fee more than five times over for the median client. The data indicates a median estimated tax benefit-to-fee ratio of 5.5x, demonstrating that for young investors with long time horizons, the software generates significant after-tax yield enhancements.

Wealthfront extends its tax dominance through the integration of Direct Indexing (previously branded as Stock-Level Tax-Loss Harvesting). Rather than buying a monolithic S&P 500 ETF (such as VOO or SPY), Direct Indexing involves the algorithmic purchasing of the actual individual constituent stocks that comprise the index. This granular approach allows the software to harvest losses on individual declining equities (e.g., harvesting a loss on an underperforming tech stock) even if the broader macro index is trading upwards. This intra-index volatility harvesting generates exponentially more tax alpha than standard ETF-level TLH.

- Nasdaq-100 Direct: Introduced in late 2025, this product requires a low $5,000 minimum and charges an aggressive 0.12% advisory fee. It directly indexes the innovative tech sector, providing vast harvesting opportunities due to individual tech stock volatility.

- S&P 500 Direct: Requires a $5,000 minimum and charges an industry-low 0.09% advisory fee.

- US Total Market Direct Indexing: Requires a $100,000 minimum. This sophisticated portfolio utilizes a blend of individual stocks and ETFs to mimic the broader global market while maximizing constituent-level TLH across mid and small-cap sectors.

Compared to third-party optimization overlays like PortfolioPilot or Frec, Wealthfront automates the execution directly inside its managed portfolios, resulting in zero user friction, whereas competitors often require users to manually execute suggested compliant swaps at external brokerages. While Frec offers more granular customization (allowing the exclusion of specific sectors or 10 individual stocks), Wealthfront’s seamless integration remains the premium choice for hands-off automation.

Betterment: Algorithmic Efficiency Without Direct Indexing

Betterment also provides robust, fully automated TLH across all of its taxable accounts with zero minimum balance requirements, ensuring novice investors can immediately begin compounding tax benefits. Betterment’s algorithm dynamically monitors accounts daily for harvesting opportunities, automatically executing trades to capture losses while carefully navigating wash-sale rules across the client’s interconnected, multi-goal sub-portfolios.

However, Betterment suffers a major competitive disadvantage because it does not offer Direct Indexing capabilities. Tax-loss harvesting is executed strictly at the macro ETF level. While ETF-level TLH is highly effective during broad market downturns and recessions, it is mathematically inferior to stock-level direct indexing during periods of high intra-market dispersion. For instance, in a flat market where the S&P 500 is unchanged, Betterment’s ETF-level TLH cannot harvest any losses, whereas Wealthfront’s Direct Indexing can harvest losses on the 200 stocks within the index that declined, offsetting gains from the 300 stocks that rose.

Schwab: High Hurdles and Manual Execution Friction

Schwab Intelligent Portfolios significantly lags its independent financial technology competitors in tax optimization accessibility and sophisticated execution. TLH is not a democratized feature available to all users; instead, Schwab enforces a stringent $50,000 minimum invested balance requirement per eligible taxable account to unlock the algorithm. This high barrier to entry effectively locks out younger accumulators and mass-market investors from realizing early-compound tax benefits.

Furthermore, TLH is not active by default upon account creation. Clients must manually navigate their portfolio settings and actively choose to activate the feature. When finally activated, Schwab’s algorithm utilizes secondary “alternate” ETFs to rotate capital into during the mandatory 30-day wash-sale window. While effective at a basic level, the required $50,000 minimum, the necessity of manual activation, the lack of Direct Indexing capabilities, and the presence of the uninvested cash drag make Schwab an objectively inferior platform for investors seeking maximum tax alpha.

Table 2: Comparative Tax Optimization Methodologies

| Feature | Wealthfront | Betterment | Schwab Intelligent Portfolios |

|---|---|---|---|

| ETF-Level TLH | Yes (Daily, Automated) | Yes (Automated) | Yes (Automated, manual activation) |

| TLH Minimum Balance | $0 (Available to all) | $0 (Available to all) | $50,000 minimum per account |

| Direct Indexing (Stock-Level TLH) | Yes (S&P 500, Nasdaq-100, US Total Mkt) | No | No |

| Direct Indexing Fees | 0.09% - 0.25% based on index | N/A | N/A |

Alternative Assets, ESG Integration, and Cryptocurrency Exposures

As the pure equity-and-bond allocation paradigm has commoditized, automated platforms have sought to differentiate themselves through highly specialized sub-portfolios, focusing aggressively on Socially Responsible Investing (SRI) and alternative asset exposure to capture younger demographics.

Environmental, Social, and Governance (ESG) Offerings

Values-based investing remains a core component for modern automated platforms, despite broader macroeconomic backlashes against ESG greenwashing and political scrutiny that saw massive capital outflows from ESG funds in late 2025.

Betterment offers three distinct, highly curated SRI/ESG portfolios: Broad Impact, Climate Impact, and Social Impact. In January 2026, Betterment executed strategic, fiduciary-led updates to its SRI glide paths. Responding to market volatility and yield curve shifts, Betterment smoothed the de-risking algorithms across all three of its SRI portfolios by increasing exposure to short-term U.S. Treasuries. This mechanical adjustment buffers the portfolios against equity shocks as clients approach their target withdrawal dates. Betterment’s SRI integration is highly structured; clients select the pre-built thematic portfolio, and Betterment controls the underlying ESG ETF constituents.

Wealthfront approaches SRI with extreme architectural flexibility. Rather than locking users into a single, rigid ESG mandate, Wealthfront allows users to either select a pre-built SRI portfolio or manually swap out standard, conventional ETFs for socially responsible alternatives within any custom portfolio they build. This modularity empowers the investor to apply ESG filters strictly to the asset classes they care about, incurring no additional advisory fee for the customization.

Schwab Intelligent Portfolios is noticeably deficient in this area.

It does not offer dedicated, pre-built ESG or SRI portfolios within its automated wrapper. Socially conscious investors utilizing Schwab must rely entirely on the platform’s rudimentary exclusion feature, which allows the manual exclusion of up to three specific ETFs, attempting to strip out undesirable asset classes (like fossil fuels) piecemeal rather than utilizing dedicated ESG screening funds.

6.2 Cryptocurrency and Alternative Assets

The integration of highly volatile cryptocurrency into fiduciary robo-advisory accounts requires navigating complex regulatory frameworks and risk-management protocols.

Betterment previously offered a direct cryptocurrency trading platform, but shuttered that specific service in late 2024 amidst regulatory ambiguity. Pivoting effectively for 2026, Betterment now allows clients to invest in a dedicated, automated Crypto ETF portfolio comprised entirely of spot Bitcoin and Ethereum ETFs. In early 2026, Betterment conducted a major rebalance of this portfolio, structurally increasing the Bitcoin allocation and proportionally decreasing the Ethereum allocation to perfectly align with their respective global market capitalization weights. Simultaneously, Betterment shifted the underlying holdings to newly approved, lower-cost ETF providers, successfully reducing the portfolio’s weighted average expense ratio drag by a notable 0.10%.

Wealthfront does not support direct spot trading of crypto tokens on its platform. Instead, users can allocate a restricted percentage of their overall Taxable or IRA accounts into specific iShares Bitcoin and Ethereum ETFs, or legacy crypto trusts like Grayscale. Notably, due to the extreme volatility and complex wash-sale rulings pending regarding digital assets, Wealthfront explicitly excludes cryptocurrency ETF holdings from its automated tax-loss harvesting algorithms, ring-fencing them from the broader tax alpha generation.

7. Fixed Income Engineering in a Shifting Yield Curve

The macroeconomic environment of 2025 and 2026, characterized by volatile interest rate cuts, shifting geopolitical tensions, and debates surrounding artificial intelligence market caps, forced automated advisors to heavily innovate their fixed-income offerings to optimize yields and manage duration risk.

Wealthfront has aggressively positioned itself as a leader in fixed-income yield maximization. The firm launched the Automated Bond Portfolio, a diversified vehicle targeting a 4.11% to 4.14% yield (as of early 2026) using an optimized blend of corporate bonds, floating-rate bonds, and tax-advantaged Treasury ETFs, charging the standard 0.25% advisory fee. More innovatively, Wealthfront introduced the Automated Bond Ladder, charging a reduced 0.15% advisory fee. Rather than buying bond ETFs, which never mature and are subject to continuous net asset value fluctuations, this algorithmic strategy purchases individual U.S. Treasury bonds with staggered maturity dates. This ladders the capital, effectively locking in current high yields and neutralizing interest rate duration risk if held to maturity, providing a highly sophisticated, institutional-grade fixed-income solution to retail clients.

Betterment also updated its strategic fixed-income approach in 2026. Across its non-SRI portfolios (Core, Innovative Technology, Value Tilt, and Flexible), Betterment structurally added an actively managed core bond fund to its algorithm. This strategic inclusion was designed to expand global bond market exposure beyond passive indices, utilizing active management to navigate the complex, shifting yield curves and enhance risk-adjusted returns during periods of anticipated monetary policy transitions.

8. Liquidity Ecosystems and Cash Management Banking Equivalents

The war for retail deposits has led robo-advisors to function increasingly as quasi-banks, utilizing vast sweep networks to provide massive Federal Deposit Insurance Corporation (FDIC) insurance limits and highly competitive Annual Percentage Yields (APYs).

Wealthfront’s flagship liquidity product is the Wealthfront Cash Account, which requires merely a $1 minimum to open. It operates by sweeping uninvested cash nightly to a broad network of partner banking institutions (Program Banks). By distributing the capital across multiple charters, Wealthfront aggregates FDIC insurance up to $8 million (for joint accounts), far exceeding the standard $250,000 limit. Functionally, the account operates identically to a premium checking account, offering a Wealthfront Visa debit card, fee-free in-network ATM access, routing numbers for direct deposit, and integration with the Real-Time Payments (RTP) network and FedNow service for same-day withdrawal capabilities. A major feature update deployed across late 2025 and 2026 was Dividend Sweeping, an automation that identifies dividends generated within the investing portfolios and immediately sweeps them into the high-yield Cash Account, effectively creating a compounding source of passive income.

Betterment offers a bifurcated liquidity system: Betterment Cash Reserve for high-yield savings and Betterment Checking for daily transactional velocity. Cash Reserve provides up to $2 million in FDIC insurance ($4 million for joint accounts) through its own consortium of Program Banks. Betterment Checking, provided and issued via nbkc bank, offers no APY on balances, but compensates by reimbursing all ATM fees globally and covering the Visa 1% foreign transaction fee everywhere Visa is accepted. To incentivize high-net-worth consolidation, Betterment Premium users receive an exclusive +0.25% APY boost on all their Cash Reserve balances.

As previously analyzed, Schwab’s cash component is automatically held at Charles Schwab Bank. While fully FDIC insured up to standard limits, the APY generated on these swept funds is generally lower than the independent high-yield alternatives offered by Betterment or Wealthfront. This lower yield is structurally necessary, as the net interest margin captured by Schwab serves to subsidize and cover the costs of its zero-fee portfolio management model.

Table 3: Cash Management and Liquidity Features

| Feature | Wealthfront Cash Account | Betterment Cash Reserve / Checking | Schwab Bank Sweep |

|---|---|---|---|

| Minimum Balance | $1 | $0 | N/A (Part of $5k minimum) |

| FDIC Insurance Limit | Up to $8M (Joint) via Program Banks | Up to $4M (Joint) via Program Banks | $250,000 (Standard) |

| Checking Features | Debit card, RTP network, Direct Deposit | Separate Checking account, Global ATM fee reimbursement | Basic sweep; separate Schwab checking available |

| Premium Yield Boosts | No | +0.25% APY boost for Premium clients | No |

9. Jurisdictional Constraints and Expatriate Wealth Management: The Nepal Use Case

A critical and highly complex area of inquiry for global investors is the jurisdictional availability of U.S.-domiciled automated portfolios. The global financial regulatory framework—specifically the rigorous implementation of the Foreign Account Tax Compliance Act (FATCA) and international Anti-Money Laundering (AML) directives—has imposed severe, costly compliance and reporting burdens on U.S. financial institutions. Consequently, servicing non-U.S. residents and American expatriates living abroad has become highly restricted, resulting in widespread account closures across the industry.

9.1 The Strict Domestic Firewalls of Betterment and Wealthfront

Independent financial technology firms, prioritizing lean operations and domestic scale, operate with strict geographic and regulatory geofencing.

Betterment explicitly states in its 2026 legal disclosures that it operates exclusively within the borders of the United States. For overarching regulatory reasons, Betterment cannot and will not accept international customers residing outside the U.S. This restriction is absolute and includes U.S. citizens who are residing and/or working abroad (with incredibly narrow, specific exceptions made only for active U.S. military personnel utilizing valid APO addresses). Opening a Betterment account legally requires a permanent U.S. residential address, a valid U.S. Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), and a linked checking account from a U.S.-chartered bank. Furthermore, Betterment actively polices this by geoblocking application or login access from foreign IP addresses; therefore, an investor attempting to access the platform from Nepal in 2026 would be systematically blocked by the server infrastructure.

Wealthfront enforces identical, uncompromising geographic restrictions. Its backend banking infrastructure, which relies heavily on domestic partners like Green Dot Bank and UMB, is entirely U.S.-centric. Wealthfront accounts cannot be established by non-U.S. residents, and the firm does not possess the international compliance apparatus necessary to navigate foreign securities laws or FATCA reporting requirements.

9.2 Schwab One International: Global Access with Caveats

For international investors—including residents of nations such as Nepal—Charles Schwab represents the only viable institutional pathway among the three platforms evaluated, though securing access to the specific automated Intelligent Portfolios product requires nuanced navigation and acceptance of regulatory friction.

Schwab operates a dedicated division and product line known as the Schwab One International Account, designed specifically for non-U.S. residents and expatriates seeking access to U.S. equities and broader global markets. This account permits investors to trade foreign securities online in real-time across 12 top global markets, settling transactions in 7 local currencies. However, utilizing this account introduces significant complexities:

- Taxation (Chapter 3 Withholding): Non-U.S.

taxpayers opening a Schwab International account are immediately subject to Chapter 3 dividend withholding regulations. Any U.S.-sourced dividend income generated within the portfolio will face a mandatory flat withholding tax (frequently 30%, unless explicitly reduced by a bilateral tax treaty between the U.S. and the investor’s country of residence). This tax is automatically deducted by Schwab at the source before the dividend hits the account, significantly reducing the compounding yield of the portfolio for foreign investors.

- Country Eligibility (Nepal): Schwab strictly regulates exactly which global jurisdictions are permitted to open accounts, driven by evaluations of local securities laws, capital controls, and regional AML risk profiles. While Schwab supports a vast array of countries, specific eligibility for residents of Nepal is not blanketly guaranteed. Prospective clients must navigate the Schwab online application portal’s country-selection residency test to verify current status, as compliance frameworks shift rapidly. Many developing nations require burdensome paper applications, and some face outright restrictions.

- Product Availability Limitations: Critically, even if a Nepalese resident successfully clears AML checks and opens a Schwab One International brokerage account, the Schwab Intelligent Portfolios robo-advisory service itself may not be cross-compatible with that foreign residency status. Schwab’s legal disclosures repeatedly and explicitly stipulate that “not all products, services, or investments are available in all countries,” and fiduciary advisory services governed by the SEC often strictly restrict non-resident access to avoid violating foreign financial advice solicitation laws. Foreigners looking to build automated wealth are frequently forced to abandon the robo-advisor wrapper entirely, instead utilizing the Schwab international brokerage account to manually purchase and self-direct a portfolio of global ETFs (which carry $0 online commissions at Schwab) to manually replicate a robo-portfolio structure.

Ultimately, for a resident of Nepal seeking automated wealth management in 2026, the modern financial technology platforms of Betterment and Wealthfront are entirely inaccessible due to absolute regulatory firewalls. Charles Schwab represents the only institutional gateway, but establishing an account requires navigating complex cross-border compliance procedures, accepting heavy U.S. dividend tax withholding, and potentially forfeiting access to the algorithmic Intelligent Portfolios wrapper in favor of self-directed global trading.

Strategic Conclusions and Platform Suitability

The maturation of the automated wealth management landscape in 2026 forces retail investors to critically align their capital with the platform that best matches their financial complexity, behavioral tendencies, and geographic domicile. The commoditization of basic ETF asset allocation means that the actual, tangible value of a robo-advisor is now derived entirely from its proprietary tax optimization software, its fixed-income structuring capabilities, and the subtle mechanics of its fee architecture.

Wealthfront definitively emerges as the premier platform for the mathematically rigorous, hands-off wealth accumulator. Its unyielding commitment to software optimization over human interaction allows it to offer the most sophisticated, high-yielding tax-loss harvesting mechanisms in the retail market. The widespread availability of Direct Indexing (across the S&P 500 and Nasdaq-100) at remarkably low entry minimums ($5,000) provides structural tax alpha that mathematically offsets the flat 0.25% advisory fee, particularly in volatile market environments. For investors prioritizing aggressive, daily tax optimization, granular ETF and sector customization, and automated bond laddering without the desire for human financial planning, Wealthfront is the definitive institutional choice.

Betterment successfully claims the mantle for goal-oriented investors, novice accumulators requiring behavioral guardrails, and affluent individuals seeking human fiduciary validation. Betterment’s flawless implementation of fractional share trading across all portfolios ensures absolute cash efficiency, leaving zero capital uninvested. Its deep architectural integration of distinct sub-goals and automated, time-horizon-based glide paths simplifies complex financial planning for major life events. Crucially, following Schwab’s abandonment of the hybrid advisory model in early 2026, Betterment Premium stands alone as the paramount option for investors with over $100,000 who are willing to pay an explicit 0.65% fee to secure unlimited access to Certified Financial Planners.

Schwab Intelligent Portfolios occupies a highly specific, yet massive, market niche: the fiercely fee-averse investor operating in a low-interest-rate environment, or the existing Schwab brokerage client seeking platform consolidation. The optical allure of a zero explicit advisory fee is psychologically powerful. However, sophisticated investors must recognize and calculate the opportunity cost of the mandatory 6% to 30% cash allocation, which effectively serves as a heavy implicit AUM fee during equity bull markets. Furthermore, Schwab’s steep $50,000 minimum balance requirement merely to unlock basic, non-stock-level tax-loss harvesting severely limits its utility for young accumulators attempting to maximize early compounding. Nevertheless, for international investors—such as expatriates or those residing in eligible foreign jurisdictions—Schwab’s vast global infrastructure and Schwab One International account provide the only realistic, legally compliant gateway to U.S. institutional wealth management, despite the heavy regulatory and tax withholding burdens involved.

In closing, the selection of an automated advisor in 2026 transcends the mere comparison of generic rebalancing algorithms. It is a highly strategic, long-term decision between Wealthfront’s tax-centric direct indexing dominance, Betterment’s fractional goal-based pathing and human fiduciary access, and Schwab’s zero-fee, cash-heavy brokerage integration. Integrating these specific architectural advantages against the investor’s individual tax bracket, timeline, and international residency status remains the ultimate determinant of long-term net yield and successful wealth preservation.