Cheapest Remote Startup Incorporation: Atlas Alternatives Guide

The contemporary digital economy has fundamentally democratized the process of launching a technology startup, allowing founders from across the globe to access the United States market, venture capital ecosystems, and advanced financial infrastructure without requiring physical residency. For years, Stripe Atlas has served as the default gateway for remote and international founders seeking to establish a U.S. corporate entity rapidly. However, as the global entrepreneurial ecosystem has matured throughout the 2020s, a multitude of highly specialized alternatives have emerged. These platforms offer nuanced advantages regarding cost-efficiency, ongoing compliance management, post-incorporation legal support, and integration with modern financial technology. Navigating this landscape requires more than simply selecting a formation service; it demands a strategic understanding of corporate jurisprudence, tax structuring, regulatory compliance, and cross-border banking.

This comprehensive report provides an exhaustive analysis of the most cost-effective and strategic methodologies for incorporating a remote technology startup in 2026. It dissects jurisdictional choices between onshore and offshore entities, evaluates leading incorporation platforms against the Stripe Atlas standard, outlines the hidden costs of registered agents and virtual infrastructure, and provides a rigorous assessment of post-incorporation tax compliance, the shifting landscape of federal beneficial ownership reporting, banking access, and capital repatriation for non-resident founders.

Jurisdictional Architecture: Selecting the Optimal Corporate Domicile

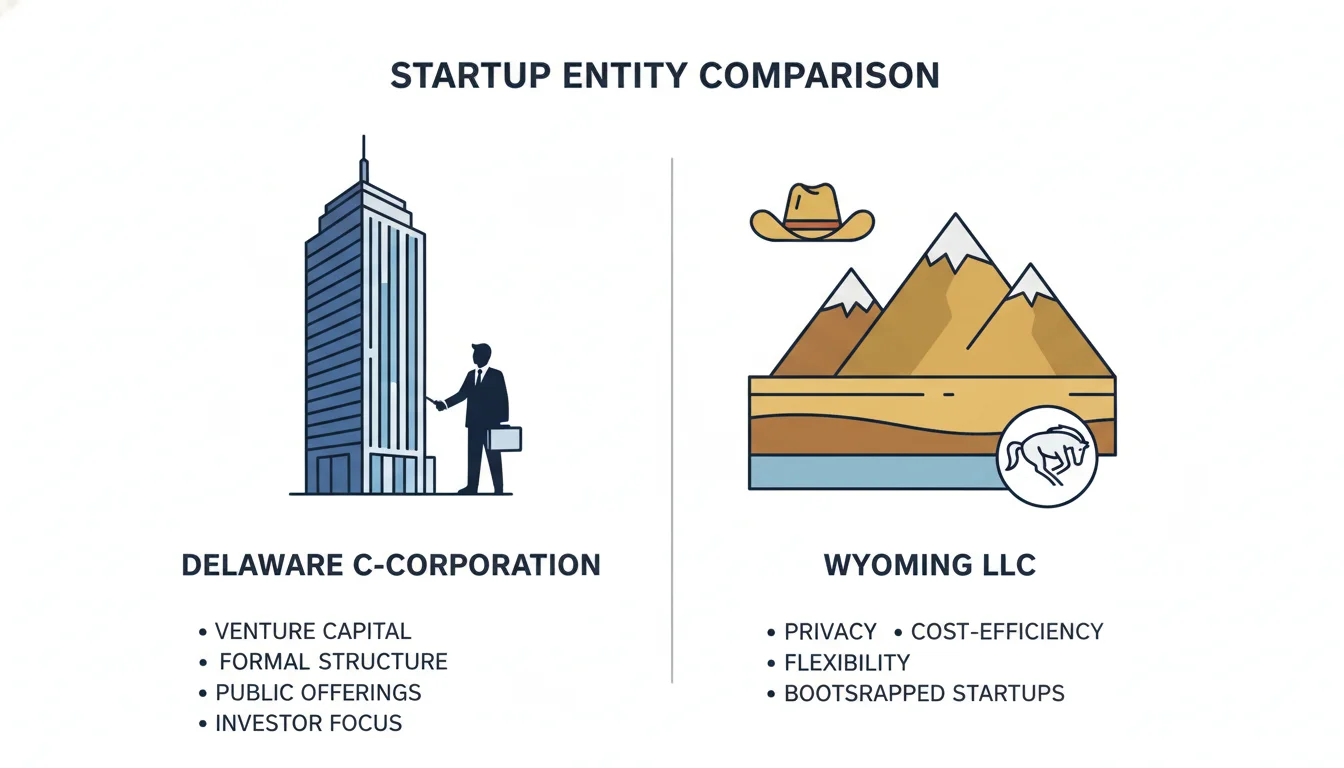

The foundational decision for any remote tech startup is the selection of the appropriate legal entity and the geographical state of incorporation. While the United States consists of fifty distinct corporate jurisdictions, alongside numerous offshore options, the optimal choice for a remote, scalable technology startup almost universally narrows down to three distinct pathways: a Delaware C-Corporation, a Wyoming Limited Liability Company, or an offshore holding entity such as a British Virgin Islands (BVI) company. The selection dictates not only initial capital requirements but also long-term taxation, governance rigidity, and investor compatibility.

The Delaware C-Corporation: The Uncontested Venture Capital Standard

Delaware remains the undisputed gold standard for technology startups seeking to raise institutional venture capital, with over 68% of Fortune 500 companies incorporated within its jurisdiction. The preference for Delaware is not driven by geographic proximity or immediate tax savings, but rather by its sophisticated corporate legal framework. Delaware features the highly revered Court of Chancery, a specialized judicial body that resolves corporate disputes using judges highly versed in business law rather than relying on civil juries. This provides unparalleled legal predictability, a feature that institutional investors mandate to protect their deployed capital.

Furthermore, venture capital firms are typically structured as pass-through entities, such as limited partnerships, and are legally or structurally prohibited from investing in Limited Liability Companies. Investing in a pass-through LLC would force the venture capital fund to distribute what is known as “phantom income” to its limited partners, thereby creating personal tax liabilities for those partners without corresponding cash distributions to pay those taxes. Therefore, a C-Corporation—which acts as a separate, distinct taxable entity that retains its own earnings and pays its own corporate taxes—is a structural necessity for any startup aggressively pursuing angel investment or venture backing. Incorporating as an LLC when the primary goal is venture capital is widely considered an unforced error that signals amateurism to institutional investors, ultimately necessitating a costly conversion process later.

The Wyoming LLC: Unmatched Operational Efficiency and Founder Privacy

For bootstrapped startups, solo founders, digital nomads, or businesses operating on a pure cash-flow model without the immediate intention of raising venture capital or issuing complex equity compensation, a Wyoming LLC presents a highly cost-effective and private alternative. Wyoming pioneered the LLC structure in the United States and offers a highly favorable tax climate characterized by the complete absence of state corporate income taxes, personal income taxes, and franchise taxes.

Beyond taxation, Wyoming heavily prioritizes founder privacy. The state does not require the names of LLC members or managers to be listed on public records, allowing remote founders to operate with a degree of anonymity. Furthermore, Wyoming does not explicitly mandate an operating agreement to be filed with the state, minimizing initial bureaucratic overhead, and it provides robust asset protection through its specialized charging order laws. While Delaware also offers an LLC structure, it lacks the privacy protections of Wyoming (requiring public disclosure of member identities) and enforces a minimum annual franchise tax that Wyoming does not impose. For non-resident entrepreneurs who simply require a U.S. entity to access payment processors like Stripe or Amazon U.S., the Wyoming LLC is often the most economically rational choice.

The Offshore Alternative: The British Virgin Islands (BVI)

While U.S. incorporation is the primary focus for technology startups, certain international founders operating globally without a requirement for U.S. customers may consider offshore jurisdictions. The British Virgin Islands (BVI) is a premier offshore jurisdiction, ideal for holding companies, managing international investments, and extreme asset protection. The BVI offers strong confidentiality, no corporate income tax, and straightforward compliance requirements. However, financial infrastructure has evolved rapidly, and offshore entities increasingly face severe friction when attempting to open accounts with modern financial technology platforms or global payment gateways. The implementation of global transparency standards, such as the Common Reporting Standard (CRS), has somewhat eroded the traditional secrecy of offshore havens, making the operational ease of a U.S. LLC often superior to the theoretical tax benefits of a BVI company.

State-Level Cost Comparison Matrix

The financial burden of maintaining the corporate veil varies significantly between the two dominant U.S. jurisdictions. The following table provides a comprehensive breakdown of the baseline statutory costs, independent of any third-party service fees.

| Metric | Delaware C-Corporation | Wyoming LLC |

|---|---|---|

| Initial State Filing Fee | $90 minimum (varies with stock authorization) | $100 ($102 by mail) |

| Annual Report Fee | $50 for non-exempt domestic corporations | Minimum $60 (or $0.0002 per dollar of assets in WY) |

| Annual Franchise Tax | Minimum $175 (Authorized Shares Method) or $400 (Assumed Par Value Method) | None |

| Certificate of Good Standing | $50 (short form) / $175 (long form) | Free |

| Late Filing Penalties | $200 penalty plus 1.5% interest per month | Administrative dissolution after 60 days of delinquency |

The Mathematics of Corporate Maintenance: Navigating the Franchise Tax Trap

A critical vulnerability for inexperienced remote founders incorporating in Delaware is the miscalculation of the Annual Franchise Tax. Delaware offers two distinct mathematical methods for calculating this tax, and corporations are legally permitted—and actively instructed by the state—to pay the lesser of the two amounts. Failure to understand these methods frequently results in startups receiving automated tax bills for tens of thousands of dollars, causing unnecessary panic.

Method 1: The Authorized Shares Method

The Authorized Shares Method is the default calculation applied by the Delaware Division of Corporations. This method calculates the tax liability based entirely on the total number of authorized shares listed in the company’s Certificate of Incorporation, regardless of whether those shares have actually been issued to founders or investors. The calculation follows a strict tiered structure:

- Corporations with 5,000 shares or fewer pay the minimum tax of $175.

- Corporations with 5,001 to 10,000 shares pay $250.

- For each additional 10,000 shares (or portion thereof), the tax increases by $85.

- The maximum annual tax under this method is capped at $200,000.

Many technology startups, acting on standard legal advice to prepare for future employee equity pools and venture capital rounds, automatically authorize 10,000,000 shares at formation. Under the Authorized Shares Method, a corporation with 10,000,000 authorized shares will generate a first-year franchise tax bill exceeding $85,000. For a pre-revenue remote startup, this default assessment appears catastrophic.

Method 2: The Assumed Par Value Capital Method

To avoid this exorbitant tax burden, startups with a high number of authorized shares but relatively low asset values must actively calculate their liability using the Assumed Par Value Capital Method. To utilize this method, the corporation must accurately report all issued shares (including treasury shares) and total gross assets as reported on U.S. Form 1120, Schedule L, on their Annual Franchise Tax Report. The minimum tax utilizing this method is $400, and the rate is assessed at $400 per million dollars (or portion thereof) of assumed par value capital.

The calculation involves a precise multi-step process.

First, the corporation determines the “assumed par” by dividing total gross assets by total issued shares, carrying the result to six decimal places. Second, this assumed par value is multiplied by the number of authorized shares that have a par value less than the assumed par. Third, for authorized shares with a par value greater than the assumed par, those shares are multiplied by their respective statutory par value. These two components are added together to produce the “assumed par value capital”. Finally, this total capital figure is rounded up to the next million (if it exceeds $1,000,000), divided by 1,000,000, and multiplied by $400 to determine the final tax liability.

For example, if a Delaware startup has 15,000,000 authorized shares with a par value of $0.01, $1.2 million in gross assets, and 10,000,000 issued shares, the assumed par value is $0.12 ($1.2 million divided by 10 million). Multiplying this $0.12 by the 15,000,000 authorized shares yields an assumed par value capital of $1.8 million. Rounding up to the next million yields $2 million. Dividing by 1 million and multiplying by $400 results in a total franchise tax due of only $800. By utilizing this method, startups successfully suppress their franchise tax from tens of thousands of dollars to a highly manageable operational expense, highlighting the critical importance of understanding corporate finance mechanics before utilizing cheap automated filing tools.

Premium and Equity-Integrated Incorporation Platforms

Stripe Atlas established the modern paradigm of “incorporation as a service” by bundling legal formation, EIN acquisition, and immediate banking access into a single $500 product. In 2025 alone, Atlas incorporated one in five Delaware C-Corps, enabling 20% of its users to land their first paying customer within 30 days of formation due to seamless payment integration. However, the platform operates on a rigid template model and has drawn criticism within founder communities for essentially abandoning entrepreneurs to navigate complex post-incorporation compliance alone. In 2026, founders seeking the most cost-effective or comprehensive solutions must evaluate a diverse spectrum of alternatives that cater to specific growth trajectories.

The Silicon Valley Standard: Clerky

Clerky is widely recognized as the premium platform of choice for highly scalable, venture-backed startups, notably functioning as the preferred software for alumni of top-tier accelerators like Y Combinator. Founded by former Silicon Valley attorneys, Clerky focuses almost exclusively on generating “attorney-grade” paperwork that prevents catastrophic due diligence failures during future fundraising rounds. The platform’s core philosophy is that saving a few hundred dollars on automated formation is irrelevant if a flawed capitalization table results in a massive tax bill or deters a Series A investor.

Unlike Stripe Atlas’s one-time fee model, Clerky offers two sophisticated pricing architectures tailored to startup funding life cycles. The “Pay-Per-Use” model starts with a $427 fee for Delaware incorporation, which includes the $203 expedited state filing fees and the $125 first-year registered agent fee. Subsequent actions, such as post-incorporation setup ($299), adopting a stock plan ($199), or issuing individual SAFEs ($9) and Convertible Notes ($19), are billed a la carte.

Alternatively, the “Company Lifetime Package” requires a one-time fee of $819. This comprehensive package includes initial incorporation, post-incorporation setup, stock plan adoption, foreign qualification support, and unlimited issuance of standard legal documents (NDAs, SAFEs, convertible notes, board consents) for the duration of the company’s existence. For startups anticipating rapid growth, aggressive hiring, and frequent milestone fundraising, Clerky’s Lifetime Package represents the most cost-effective long-term legal infrastructure available, drastically undercutting the thousands of dollars typically required for traditional hourly legal counsel.

Cap Table and Equity Management Platforms: Gust Launch and Capbase

Startups that require immediate, complex equity distribution among multiple co-founders, early employees, and advisors may benefit from platforms that merge the act of incorporation directly with advanced capitalization table software.

Gust Launch operates on a recurring subscription model starting at $450 per year for its “Start” plan. This baseline tier includes Delaware C-Corporation formation, EIN acquisition, corporate bylaws, electronic stock issuance, and an automatically managed digital cap table. Gust Launch differentiates itself by locking founders into higher software tiers as they scale. The “Accelerate” plan at $1,250 per year introduces unlimited SAFEs, convertible notes, and contractor agreements, while the “Raise” plan at $3,500 per year unlocks full option plan generation, board approvals, and complex 409A valuations necessary for issuing equity compensation in compliance with IRS regulations.

Capbase provides a similar end-to-end “Startup OS” methodology, charging a flat $999 yearly fee. This fee encompasses incorporation, direct bank account integration, employee stock plan management, automated due diligence document rooms, and ongoing compliance calendars. While these platforms centralize operations, founders must be cautious of the vendor lock-in created by marrying their foundational corporate legal structure to a high-cost recurring software subscription.

Specialized Compliance Engines and Lean Alternatives

While venture-track startups gravitate toward Clerky or Gust, non-resident founders bootstrapping remote operations prioritize immediate market access, specialized support for foreign nationals, and the absolute minimization of upfront capital.

The “Business-in-a-Box” Models: Doola and Firstbase

For international founders, navigating the U.S. bureaucracy without a Social Security Number (SSN) is incredibly fraught. Platforms like Doola and Firstbase have engineered specific workflows to alleviate these exact pain points.

Doola positions itself as a comprehensive platform tailored explicitly for non-U.S. residents looking to penetrate the U.S. market. Priced starting at $297, Doola actively assists international entrepreneurs in navigating the complexities of acquiring an EIN without an SSN, establishing a U.S. mailing address, and opening compliant bank accounts. Doola’s primary advantage over Stripe Atlas lies in its hands-on customer support architecture, tax compliance tracking, and specialized knowledge of the friction points faced by foreign nationals.

Firstbase caters to a similar demographic, offering the “Firstbase Start” package for a one-time fee of $399. This covers standard incorporation in either Delaware or Wyoming, expedited EIN setup, and basic legal documentation. However, Firstbase relies heavily on generating recurring revenue through its “Firstbase Agent (Autopilot)” service, which costs $299 annually per state to manage registered agent duties, automated state compliance reminders, and annual reports. While the software interface is highly streamlined, independent evaluations and community reviews have frequently highlighted severe customer support delays, hidden fees related to state franchise taxes not included in the Autopilot subscription, and instances of compliance failures.

The Ultra-Lean DIY Approach: Bizee and Northwest Registered Agent

For founders prioritizing absolute cost-minimization, utilizing commercial registered agent services to file standard incorporation paperwork presents the cheapest possible pathway to establishing a U.S. entity.

Bizee (formerly Incfile) aggressively targets the bottom of the market by offering a foundational incorporation package for $0, requiring the founder to pay only the mandatory state filing fees. Crucially, this zero-dollar package includes the first year of registered agent service for free. Upon renewal in the second year, the registered agent service costs $119 annually. While Bizee is undeniably the cheapest way to file articles of incorporation, the company relies heavily on upselling users on EIN acquisition, operating agreement templates, and banking introductions—tasks that informed founders can easily execute themselves for free.

Northwest Registered Agent operates on a slightly different philosophy, highly regarded for its strict privacy policies (“Privacy by Default”) and superior, U.S.-based customer support. Northwest charges a transparent $39 formation service fee (plus state fees) and includes the first year of registered agent service. Subsequent years are billed at a highly predictable $125 annually, with no hidden price hikes or aggressive upsell tactics. For privacy-conscious, budget-aware founders who want dependable service without the bloat of a “Startup OS,” Northwest represents the optimal balance of cost and reliability.

Open-Source and Free Legal Frameworks

Startups that elect to use bare-bones formation services like Northwest or Bizee often find themselves lacking the complex legal agreements (NDAs, IP Assignments, Bylaws) provided by premium platforms like Clerky.

However, founders do not necessarily need to pay a premium software provider to access top-tier legal templates.

Several elite global law firms have open-sourced their standard startup legal documents to act as loss-leaders and build goodwill within the entrepreneurial community. Cooley LLP, a preeminent firm representing thousands of tech startups, operates “Cooley GO,” a free web portal featuring robust document generators. Founders can utilize Cooley GO to generate full incorporation packages (for Delaware entities), term sheets, employment agreements, and IP assignment documents entirely for free. Similarly, Orrick, Herrington & Sutcliffe offers “Orrick Total Access,” another repository of free, attorney-grade startup documentation.

While these free resources are invaluable, relying on them requires the founder to act as their own project manager, ensuring that documents are properly executed, signed, and stored. Unlike Clerky or Gust Launch, which provide automated workflows and compliance reminders, utilizing Cooley GO means the founder assumes the entire administrative burden. This approach is highly cost-effective but introduces a margin for human error if the founder fails to properly file the generated documents with the state or the IRS.

Architecting the Virtual Infrastructure for Non-Residents

Incorporating a remote business requires more than legal filings; it necessitates the establishment of a localized U.S. operational presence to satisfy state regulatory compliance, receive service of process, and successfully navigate the stringent Know Your Customer (KYC) protocols of modern financial institutions.

The Registered Agent Imperative

Every U.S. corporate entity is legally mandated to maintain a registered agent within its state of formation. The registered agent is a designated person or entity physically located in the state, authorized to receive legal documents (service of process), tax notices, and official state correspondence during standard business hours. For non-resident founders or digital nomads without a fixed U.S. address, acting as their own registered agent is geographically impossible and legally non-compliant, necessitating the hire of a third-party service.

The pricing models of standalone registered agents vary considerably. Premium legacy providers like LegalZoom charge an exorbitant $249 annually, an unnecessary premium for what is essentially a commoditized mail-forwarding service. Mid-tier providers like ZenBusiness charge $199 annually. The most cost-effective and reliable standalone solutions are Northwest Registered Agent ($125/year), Harbor Compliance ($99/year, featuring same-day document delivery), and Delaware Registered Agent Service ($49/year, strictly limited to Delaware entities). Selecting a dedicated, low-cost registered agent prevents startups from falling victim to the predatory subscription renewals often embedded in “free” online formation platforms.

Virtual Mailboxes and Physical Business Addresses

A critical distinction that causes endless frustration for international founders is that a registered agent address is generally unacceptable for banking KYC or establishing merchant accounts. Financial institutions require a principal place of business address. Remote founders must therefore lease a virtual business address that provides a real street location, alongside mail scanning, forwarding, and shredding services.

Top-tier virtual mailbox providers for 2026 include:

- Anytime Mailbox: Starting at highly competitive rates of $5.99/month, offering a vast network of global and U.S. addresses managed through a centralized digital interface, ideal for digital nomads.

- PhysicalAddress.com: Starting at $7.98/month. Unlike competitors that franchise out operations to local pack-and-ship stores, PhysicalAddress owns and operates all of its real estate. This ensures significantly higher security, consistent mail handling, and unlimited cloud storage for scanned documents.

- iPostal1: Starting at $9.99/month, offering one of the largest networks with over 3,500 real street addresses. While highly flexible, service quality can vary based on the specific franchised location managing the physical mail.

U.S. Telecommunications and A2P 10DLC Compliance

A verifiable U.S. phone number is an absolute prerequisite for banking two-factor authentication (2FA), IRS communication, and interacting with domestic customers. Furthermore, the U.S. telecommunications industry has strictly implemented Application-to-Person 10-Digit Long Code (A2P 10DLC) regulations, which require businesses to register their corporate entities before they are permitted to send SMS messages to U.S. consumers.

International founders can secure U.S. numbers via Voice over Internet Protocol (VoIP) providers such as Quo, JustCall, or Surfshark. However, certain stringent fintech banks and payment processors flag VoIP numbers during automated security screening, occasionally blocking account creation. In such high-friction scenarios, maintaining a physical U.S. prepaid SIM card (such as T-Mobile or Tello) via international roaming plans ensures uninterrupted access to SMS verification codes without triggering fraud algorithms designed to block virtual numbers.

Tax Identification and the Section 83(b) Paradox

The act of receiving the filed Articles of Incorporation is merely the prologue to operating a U.S. startup. The true administrative complexities for remote and international founders emerge during the acquisition of federal tax identifiers and the filing of crucial equity tax elections.

The Employer Identification Number (EIN) Bottleneck

The Employer Identification Number (EIN) is the fundamental federal tax identifier required to open a U.S. business bank account, process payments via Stripe, and hire employees. For U.S. citizens possessing a Social Security Number (SSN), acquiring an EIN is an instantaneous, free online process via the IRS website.

For non-U.S. residents who do not possess an SSN or an Individual Taxpayer Identification Number (ITIN), the online portal is permanently inaccessible. The founder must physically complete IRS Form SS-4. The most expedient method for submission is via fax to the IRS at the designated international number, 855-641-6935. If the form is correctly formatted, the IRS will fax the official EIN assignment letter back within four to eight business days. Mailing the form to the IRS facility in Cincinnati, Ohio, is an alternative but can unnecessarily extend processing times to several weeks. Startups can outsource this process via platforms like Doola or Firstbase, or utilize a digital fax service (such as Fax.Plus) to handle the SS-4 submission independently for mere dollars, avoiding premium service upcharges.

The Section 83(b) Election: Securing the Capital Gains Advantage

When a founder receives shares in a newly formed Delaware C-Corporation that are subject to a vesting schedule (a standard requirement for venture-backed entities), the IRS treats the vesting of those shares over time as a recurring taxable event. Without intervention, the founder must pay ordinary income tax on the fair market value of the shares as they vest. If the startup experiences rapid valuation growth, this creates a catastrophic tax liability known as “phantom income“—the founder owes massive taxes on the paper value of shares they cannot yet liquidate.

Section 83(b) of the Internal Revenue Code allows the founder to proactively elect to be taxed on the fair market value of the equity at the time of the initial grant rather than as it vests. Because the value of stock at the exact moment of incorporation is typically nominal (e.g., $0.0001 per share), the immediate tax burden is practically zero. Furthermore, making the election triggers the capital gains holding period clock immediately, ensuring that future liquidity events are taxed at the much lower long-term capital gains rate rather than punishing ordinary income rates. Failing to file this document is one of the most common and devastating unforced errors a startup founder can make, often resulting in six-figure tax liabilities down the road.

The Non-Resident 83(b) Filing Paradox

The 83(b) election must be physically mailed to the IRS within a strict, unforgiving 30-day window from the date of the equity grant; there is no electronic filing option available. For non-U.S. residents who do not possess a U.S. TIN, filing the 83(b) creates a severe bureaucratic paradox. The form explicitly requires a TIN, but because acquiring an ITIN from the IRS takes months, it is functionally impossible to secure one within the 30-day window.

The prevailing legal workaround utilized by specialized startup attorneys requires the foreign founder to enter “Applied For” or simply “N/A” in the TIN field of the 83(b) election form. The form, along with a cover letter and a completed Form W-7 (Application for IRS Individual Taxpayer Identification Number), must then be sent via certified international mail to the specific Department of the Treasury IRS Service Center in Austin, Texas. Once the founder eventually secures an ITIN, a secondary, updated 83(b) form must be submitted to append the tax record. While non-residents operating entirely abroad are generally not subject to U.S. capital gains taxes, top legal counsel strongly advises filing the 83(b) regardless. It acts as an unbreakable safeguard should the founder ever relocate to the U.S. or become a U.S. tax resident during the highly unpredictable lifecycle of the company.

The FinCEN BOI Regulatory Paradigm Shift

A monumental shift in U.S. corporate compliance occurred with the implementation and subsequent revision of the Corporate Transparency Act (CTA).

The CTA originally mandated that tens of millions of small businesses report their Beneficial Ownership Information (BOI) to the Financial Crimes Enforcement Network (FinCEN) to combat money laundering, shell companies, and illicit finance. This originally applied to virtually all LLCs and C-Corps formed in the United States.

However, following fierce legal pushback and a pivotal U.S. Department of the Treasury announcement on March 2, 2025, FinCEN published an interim final rule on March 26, 2025, that completely altered the reporting landscape, providing massive relief to remote founders.

8.1 Total Exemption for Domestic Entities

Under the sweeping 2025 ruling, all entities created within the United States—previously categorized as “domestic reporting companies”—are entirely exempt from the requirement to report BOI to FinCEN. This means that a Delaware C-Corp or a Wyoming LLC formed by a remote founder now carries zero BOI reporting overhead, regardless of whether the beneficial owners are U.S. citizens or foreign nationals. FinCEN explicitly stated that it will not enforce any BOI penalties or fines against domestic entities or their beneficial owners, effectively neutralizing the most burdensome compliance requirement of the decade for U.S. startups.

8.2 Shifting the Burden to Foreign Entities

The CTA’s implementing regulations were revised to narrowly apply the definition of a “reporting company” exclusively to entities formed under the laws of a foreign country that have registered to do business in any U.S. state or tribal jurisdiction (e.g., via a process called foreign qualification).

For these foreign reporting companies, stringent deadlines remain enforced:

- If a foreign entity was registered to do business in the U.S. before March 26, 2025, it must file its BOI report by April 25, 2025.

- If a foreign entity registers in the U.S. on or after March 26, 2025, it has exactly 30 calendar days to file its initial BOI report after receiving notice that its registration is effective.

Crucially, even for these foreign reporting companies, the rule removes the requirement to report the BOI of any U.S. persons involved in the entity.

8.3 Strategic Implications for Jurisdictional Choice

This massive deregulation drastically alters the strategic math of global incorporation. Previously, some international founders preferred forming offshore entities (like a BVI company) to avoid U.S. transparency laws. However, if that offshore entity needs to register to do business in a U.S. state to access certain markets or banking, it is now subject to strict 30-day FinCEN BOI reporting. Conversely, by incorporating directly in the U.S. (via a Delaware C-Corp or Wyoming LLC), the founder creates a domestic entity that is completely exempt from FinCEN surveillance. The domestic route now paradoxically offers vastly superior privacy and less federal compliance overhead than the offshore route, cementing the U.S. LLC and C-Corp as the premier global corporate vehicles for 2026.

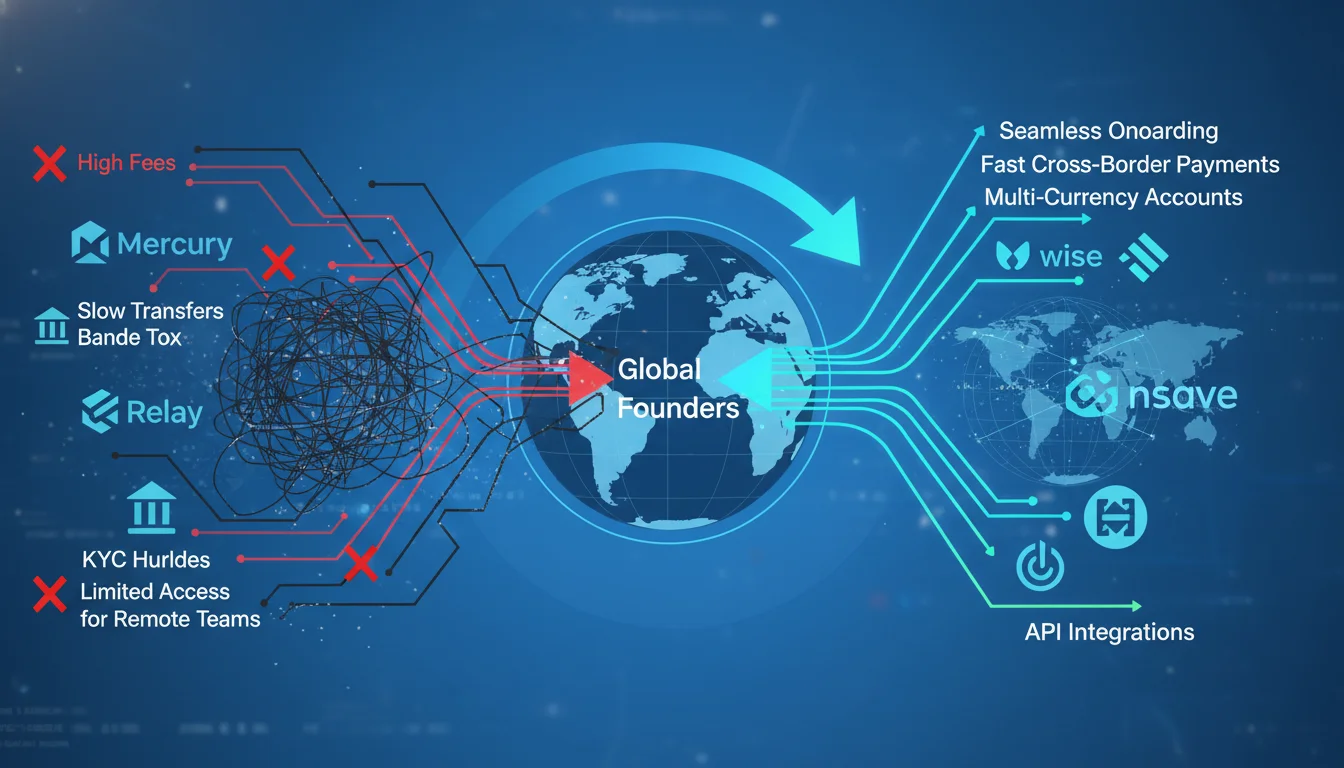

9. Architecting the Global Banking Stack

Operating a remote tech startup requires the frictionless, rapid movement of capital across borders. For U.S. residents, establishing commercial banking is a commoditized, straightforward process. For international founders, however, the U.S. banking system presents formidable barriers driven by stringent anti-money laundering (AML) protocols and the Office of Foreign Assets Control (OFAC) sanctions lists. A legally flawless Delaware C-Corp is functionally useless if it cannot open a bank account to receive customer funds.

9.1 The Retreat of the Tech Banks from Emerging Markets

Historically, fintech platforms like Mercury and Relay Financial served as the default banking layer for international tech startups. Operating as financial technology companies providing an agile “overlay” to traditional partner banks (thereby offering FDIC insurance), they enabled remote, digital account opening without requiring the founder to visit a physical U.S. branch.

However, leading into 2025 and 2026, intensified regulatory scrutiny and compliance pressures forced these platforms to severely restrict their operational footprints. Mercury, once the darling of Silicon Valley accelerators, implemented sweeping bans on founders residing in numerous jurisdictions, abruptly closing accounts for users in Bangladesh, Pakistan, Nepal, the Democratic Republic of the Congo, Nigeria, and several other nations. Mercury also paused physical and virtual card issuance to dozens of countries globally, citing regional conflicts and international regulations.

Similarly, Relay Financial maintains a strict prohibited list that explicitly bars accounts for business owners residing in Nepal, Belarus, Cambodia, and over twenty other nations. Relay also heavily restricts the sending and receiving of international wires to these regions, making it impossible to utilize for a truly global, emerging-market operation. As these primary avenues close, founders must pivot to alternative financial platforms tailored for high-friction cross-border operations.

9.2 The Vanguard of Borderless Finance: Wise Business and nsave

Founders located in restricted geographies must utilize platforms that assess risk differently than traditional U.S. bank overlays.

Wise Business Wise Business operates not as a traditional bank, but as a highly regulated Electronic Money Institution (EMI). Wise allows non-resident founders to open robust business accounts holding over 20 currencies, providing localized U.S. account details (routing and account numbers) to receive USD seamlessly via the domestic ACH network. Because Wise relies on the country from which the business is managed rather than demanding strict U.S. residency, it is significantly more accessible to founders in emerging markets. Wise charges no incoming fees for domestic ACH transfers and utilizes transparent, mid-market exchange rates, making it an economically superior choice for capital management.

nsave Emerging rapidly as a direct alternative for founders in regions aggressively abandoned by Mercury (such as Nepal, Pakistan, and Bangladesh), nsave provides a highly specialized infrastructure. Crucially, nsave allows businesses to receive incoming capital from both corporations and individuals without levying the percentage-based incoming fees characteristic of other cross-border platforms. By eliminating incoming fees and offering highly competitive foreign exchange rates upon repatriation to local currencies, nsave enables founders in high-friction environments to retain significantly more of their earned capital. For example, on a $1,000 transfer to Pakistan, utilizing nsave versus a competitor can result in the founder retaining over 11,000 PKR more due to optimized fee structures.

Payoneer Payoneer is specifically engineered to facilitate payments for freelancers, digital agencies, and global e-commerce operators interacting with large marketplaces. Like Wise, it provides local USD receiving accounts. However, Payoneer’s fee structure is generally more aggressive, frequently charging a 1% fee on incoming USD transfers, which can severely compound over time for high-volume SaaS startups.

9.3 U.S.-Centric Alternatives: Brex, Bluevine, and Novo

For founders who do maintain a U.S. presence, or reside in unrestricted, low-risk countries, the domestic fintech market remains highly competitive.

- Novo: Offers fee-free business checking integrated deeply with tools like Stripe, Shopify, and QuickBooks. It is highly favored by solopreneurs and freelancers, though it notably lacks an APY on held balances and does not support the initiation of outgoing wire transfers, which can bottleneck larger B2B payments.

- Brex: Tailored explicitly for venture-backed startups that require high-limit corporate credit cards, automated spend management, and treasury services to yield interest on idle capital. Brex is powerful but exclusionary; its strict underwriting requires substantial initial funding or demonstrated, high-velocity revenue, making it inaccessible for early-stage bootstrapped founders.

- Bluevine: Bridges the gap by offering a business checking account that yields a high APY (up to 2.0% on balances up to $250,000) and supports traditional functions like cash deposits. It acts as a comprehensive digital replacement for a traditional brick-and-mortar bank.

10. Global Payment Processors and Merchant of Record (MoR) Alternatives

Integrating a bank account is only half the revenue equation; the startup must actually process customer transactions. While Stripe is the ubiquitous payment gateway, it is not supported in every country, and it fundamentally places the burden of global tax compliance (such as calculating and remitting VAT in Europe) entirely on the startup. For remote software and digital goods companies, utilizing a Merchant of Record (MoR) is often a vastly superior, albeit slightly more expensive, alternative.

An MoR fundamentally assumes the legal liability for processing the transaction.

When a customer buys a software subscription, they are technically buying it from the MoR, which then passes the funds to the startup. Because the MoR is the legal entity executing the sale, the MoR automatically calculates, collects, and remits all global sales taxes and VAT on the startup’s behalf. This relieves the remote founder from the crushing administrative burden of registering for tax collection in dozens of foreign jurisdictions.

Leading MoR alternatives to a pure Stripe integration include:

- Paddle: A dominant payment infrastructure platform tailored purely for SaaS and software companies, offering built-in subscription management, fraud protection, and total global tax compliance.

- FastSpring: Highly robust MoR for digital goods, software, and AI tools, particularly strong at automating complex EU VAT requirements.

- Lemon Squeezy: Recently acquired by Stripe, this platform offers a highly intuitive, drag-and-drop interface for launching digital products and managing subscriptions with zero coding required, handling all tax burdens natively.

- Adyen: For enterprise-scale omnichannel retailers, Adyen operates on a transparent Interchange++ pricing model. While powerful, its complexity and fee structures are generally excessive for an early-stage remote software startup.

Capital Flow Dynamics and Emerging Market Nuances

A remote startup’s financial architecture is incomplete if the founder cannot legally inject initial capital to fund the incorporation process, or smoothly repatriate future profits back to their home country. Founders operating from emerging markets face distinct regulatory hurdles, requiring a deep understanding of evolving local banking laws and new U.S. tax legislation.

Regulatory Easing in Emerging Markets: The Nepal Case Study

Historically, countries with fragile or developing foreign exchange reserves maintained draconian controls on outward remittance, preventing founders from legally paying for services like Stripe Atlas or Clerky. However, nations are adapting to the digital economy. In Nepal, the Nepal Rastra Bank (NRB) has recently executed sweeping liberalizations to accommodate the tech sector.

Under the Fifth Amendment to the Foreign Loan and Investment Management Bylaws, implemented in late 2025, the NRB fundamentally shifted its regulatory posture. The amendment removed the requirement for prior central bank approval for foreign equity investments, shifting to a decentralized, post-transaction supervision model. Furthermore, the NRB has explicitly authorized IT firms registered in Nepal to invest up to $1,000,000 USD abroad, or 50% of their average export earnings over three years, whichever is lesser. This critical reform allows founders to legally wire funds to the U.S. to cover incorporation costs, legal counsel, and initial cloud server infrastructure without engaging in regulatory arbitrage.

For capital repatriation, the NRB directives now allow local commercial banks to directly approve the return of dividends, profits, and income from the sale of foreign-invested shares, entirely bypassing the previously centralized and severely delayed central bank review process.

The Impact of the 2026 U.S. Remittance Tax

While emerging markets are liberalizing outward capital flows, the United States has introduced new friction via the recently enacted “One Big Beautiful Bill Act,” which established a 1% federal excise tax on specific outward remittances effective January 1, 2026.

Fortunately for remote tech founders, this tax is highly targeted and easily avoided through standard digital operations. The 1% levy applies strictly to transfers funded by physical instruments—namely physical cash, money orders, and cashier’s checks sent via services like Western Union or MoneyGram. According to IRC Section 4475, standard commercial operations utilizing bank account transfers (ACH or Wire), U.S. debit/credit card payments, and cryptocurrency transfers are explicitly exempt from the tax. Therefore, remote startups paying international contractors or repatriating dividends via digital platforms like Wise Business or Airwallex will not incur this 1% penalty, provided the funding source remains purely digital.

The Hidden Costs of AI Automation in Legal Tech

As founders search for the absolute cheapest incorporation methods, many are increasingly drawn to platforms advertising “AI-automated” legal structuring. While natural language processing models can easily populate a generic set of Articles of Organization, the application of Artificial Intelligence in bespoke corporate law remains fraught with hidden operational and strategic costs.

AI models are highly proficient at filling in variable fields within templates, but they cannot yet provide the nuanced strategic counsel required to navigate complex scenarios, such as optimizing the Assumed Par Value calculation or advising on the precise tax implications of an 83(b) election for a dual-status alien. Startups relying purely on automated legal generators often incur massive downstream costs to correct botched capitalization tables, amend improper foreign qualifications, or defend against compliance audits that a human attorney would have prevented. The true cost of AI goes far beyond the cheap upfront generation fee; system integration, compliance remediation, and ongoing maintenance quickly add up. Therefore, leveraging software platforms built, actively maintained, and supported by experienced legal professionals (such as Clerky) remains economically superior to utilizing pure generative AI tools that lack fiduciary accountability and strategic foresight.

Strategic Conclusion and Operational Synthesis

The landscape of remote tech startup incorporation in 2026 is no longer defined by a single monolithic provider like Stripe Atlas, but by a highly modular, competitive ecosystem. To optimize for cost, compliance, and global scalability, founders must systematically construct a customized infrastructure stack rather than relying on generalized out-of-the-box bundles.

- Jurisdictional Targeting: Startups explicitly pursuing venture capital must select the Delaware C-Corporation. Crucially, these founders must strictly utilize the Assumed Par Value Capital Method when filing their annual reports to suppress franchise taxes from tens of thousands of dollars to the $400 statutory minimum. Bootstrapped SaaS companies, digital agencies, or cash-flow businesses should default to the Wyoming LLC to capture its $60 annual maintenance, zero state taxes, and absolute operational privacy.

- Platform Optimization: While Stripe Atlas ($500) offers unparalleled speed to revenue, it lacks post-incorporation flexibility. Clerky ($427 to $819) remains the paramount choice for ensuring VC-grade legal integrity and avoiding catastrophic due diligence failures. For the absolute lowest cost, routing incorporation directly through a highly reputable provider like Northwest Registered Agent ($39 plus state fees, locking in a predictable $125/year recurring fee) is mathematically optimal, avoiding the aggressive upsells of “free” platforms like Bizee.

- Regulatory Navigation: The complete elimination of FinCEN BOI reporting for domestic entities removes a massive compliance burden, definitively solidifying the onshore U.S. entity (Delaware or Wyoming) as vastly superior to offshore formations (like the BVI) that now trigger reporting if they attempt to operate in the U.S. Concurrently, founders must meticulously execute the Section 83(b) election via physical certified mail to Austin, Texas, within the unforgiving 30-day window, navigating the TIN absence with an “Applied For” designation to secure long-term capital gains treatment.

- Financial Resilience: As domestic fintech overlays like Mercury and Relay severely restrict their global reach to manage compliance risks, international founders must pivot to multi-currency EMI platforms. Utilizing Wise Business and nsave offers access to U.S. routing numbers, transparent mid-market FX rates, and complete immunity from the 2026 U.S. cash remittance tax, ensuring that capital flows remain frictionless regardless of the founder’s physical location.

By systematically unbundling the incorporation process, rigorously managing tax elections, and leveraging specialized cross-border financial infrastructure, a remote tech startup can establish a robust, venture-ready U.S. corporate entity for a fraction of the traditional cost, perfectly positioned to capture global capital and scale without geographic limitation.